American Assets Worth Owning

250 years ago, 56 men pledged their lives, their fortunes, and their honor to each other that they would support a common cause.

Of all the men that signed the Declaration of Independence, not one of them died with nearly as much wealth as they had when they signed. They pledged their fortunes in support of freedom and meant it. They were all wealthy men when they signed but sold down their vast fortunes to support the war against the greatest military power the world had ever seen, and each of them died poor with their fortunes scattered but their honor intact.

From the period in between the Declaration of Independence in 1776 and the ratification of the Constitution in 1787, the citizens of the newly formed country needed convincing to form a government after they had just lost a great deal of blood and treasure to abolish the old one. Alexander Hamilton was instrumental in accomplishing this task when he expressed the rationale for the Constitution, line by line, in the publication of the Federalist Papers.

Most of the text of the Federalist Papers is devoted to explaining how a central government would allow for a prosperous nation. Hamilton’s chief rationale was that money needed to be raised to build a navy. It was only a navy that would protect commerce. The States were incredibly productive and produced far more than the citizens of the US could purchase. They needed to sell their goods overseas, and a navy was a necessity to protect the merchant ships from their former colonizers and the largest naval power in the world.

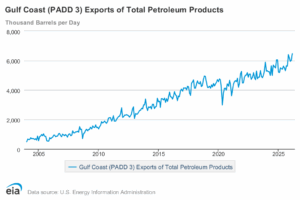

From the beginning, this country was formed with the idea that commerce leads to prosperity. Commerce has been and always will be an undertaking uniquely suited to the American experience. A notable change in the direction of that commerce is under way and under the radar. In March, the US Gulf Coast region, PADD 3, exported more petroleum products to the rest of the world than at any point in history.

The flow of commerce has been a one way trip for 50 years: our wealth flows out, and Middle East oil flows in. Thanks to the vast energy fortress the USA now possesses, as a result of generational capital contributed by our ancestors over the past 170 years of oil exploration in this country that incrementally built an energy dynamo, the flow of commerce is reversing. The rest of the world’s wealth is coming in, and refined energy products are going out.

In addition to possessing 46 billion barrels of proven reserves, the US also possesses the world’s most robust and redundant energy infrastructure: 140 refineries capable of processing any crude grade on earth, millions of miles of pipelines, coastal export terminals, and hundreds of thousands of wildcatters and independent oil producers. In its totality, our energy infrastructure is a national treasure. It is our heritage, and it is an asset bequeathed to us by past generations.

The American spirit is one of risk taking. It was the risk taking spirit that built the energy infrastructure we now possess. The spirit of risk is still evident, most readily observable in the investment preferences, between Americans and our European cousins.

While other western cultures prefer to place their savings in bonds, Americans have historically chosen a riskier, but ultimately more profitable path. We buy stocks. We always have, and we always will. There’s has been and will be more stock market crashes, but the risk taking spirit will always work its way back to the forefront of the American people’s consciousness.

While the energy infrastructure this country possesses is priceless, individual assets have a price and are for sale every day on the American stock exchanges. These are assets that I want to own. Most stocks I want to rent, but not these.

One asset I’ve owned for over a decade is $EPD. It’s the Cadillac of MLPs. It briefly went below my cost basis in the 2020 crash, and I only doubled my position. It’s one of my largest regrets that I didn’t 3x or 4x my size for the few days out of 10 years I was red on the position. But I think we’re going to get another chance this year to load up on these energy assets that we can keep forever. That chance is going to come because a wave of deflation is already on us, and I don’t think market participants are positioned for falling commodity prices.

Over the course of this summer, as global tensions ease, millions of barrels of oil will find their way back into storage. This is likely the reason the major integrated oil companies have let storage run low: they know how much oil is about to come to market after the Iran conflict winds down. If they had topped up storage in the crisis, all that oil coming to market from behind the Strait of Hormuz would crash the spot price, and that is good for no one in the oil industry.

As this oil fills storage, and the oil doomers loose their bull case, I suspect the energy names will get sold by all the traders that bought for the “war premium.” Further exacerbating the energy longs later this year should be reduced demand as the full effects of this credit bubble ending weighs on the economy.

It’s still my view that we are in the contraction phase of the business cycle, and that means we will get one chance to buy up the energy infrastructure assets that we can keep as permanent assets in our attempt to exit the working class and become part of the investor class in this country.

It’s only this country that affords opportunity to the average guy looking to make a better life for himself and his family. If this stock market offers that opportunity to me this year in an energy sell off, I plan on taking it. I’ve learned my lesson from not buying more $EPD when I had the chance, and it’s a mistake I don’t intend to make again.

It’s the energy assets I want to own because I do think the debt will still be a problem. My simple calculations give me a $45 trillion US debt level by 2028, and while I do think this country has incredible opportunity ahead, I can’t get the math to work out in a way that shows that we can manage to avoid printing money to pay the interest on the debt and roll it over on ever shortening maturity cycles.

It’s my base case that we slowly inflate the debt away over the coming decade until we can re-peg the currency and get back to a reasonable trajectory with the debt level vs growth rates. Energy assets that are irreplaceable should be major beneficiaries as the second wave of inflation that is to come becomes more entrenched in the mind of investors after a brief deflationary episode we are about to enter.

For the top tier energy infrastructure assets, I’m looking at the 200 day moving average as a place to build positions. I’ve already got $EPD, and I don’t like filling out the K-1 because I’m a speculator, not a tax guy.

So I’m looking at the other top tier pipeline companies that avoid the LLP corporate structure: $KMI, $WMB, $ENB, and $OKE.

Here’s my plan for getting into these stocks if everything unfolds this summer inline with my view:

$KMI:

$WMB

$ENB

$OKE

By: Patrick G. Full-time independent trader in Atlanta, GA.

Patrick G is a full-time trader. Worked for a decade in a money management firm as a trader for high net-worth individuals.

He invested his and his family’s net worth into gold and mining stocks before the Covid money printing. Gold and commodity runs of the past 3 years allowed Patrick to trade full-time due to his gains.

Past performance does not guarantee future results. Trading involves significant risk of loss, and individual results vary. Positions mentioned are the author’s own, disclosed for transparency — not individual investment advice.

ATTN: Serious Options Traders

There Is Just ONE Epic Trade Every Week