The End of the Market As We Know It?

We're about to enter week 3 of war with Iran. Crude oil hit shocking highs this week, while stocks hang in, right on the edge of failure.

So it's time for the 5 things you need to know.

Play this week's theme song as you read:

1. We Are on the Verge of Disaster. But There's a Catch.

The market has been a tight, frustrating mess with zero follow-through for months.

And SPY, down just 2.7% year-to-date, looks like it might be on the verge of a breakdown.

Is the 200-day moving average at $656 the next stop before a bigger collapse?

It looks like it, but there's a catch.

And of course, that catch is between now and Monday morning, we will get 48 hours of headlines.

Good luck figuring out what they'll be.

Axios reported this morning that President Trump told the G7 that Iran “is about to surrender.”

The problem is the President has a long history of hyperbole (often a big asset), and Iran shows no signs of backing down.

In fact, the Wall Street Journal reported that the Pentagon is sending more US Marines and warships to the Middle East.

The market wants resolution, ASAP.

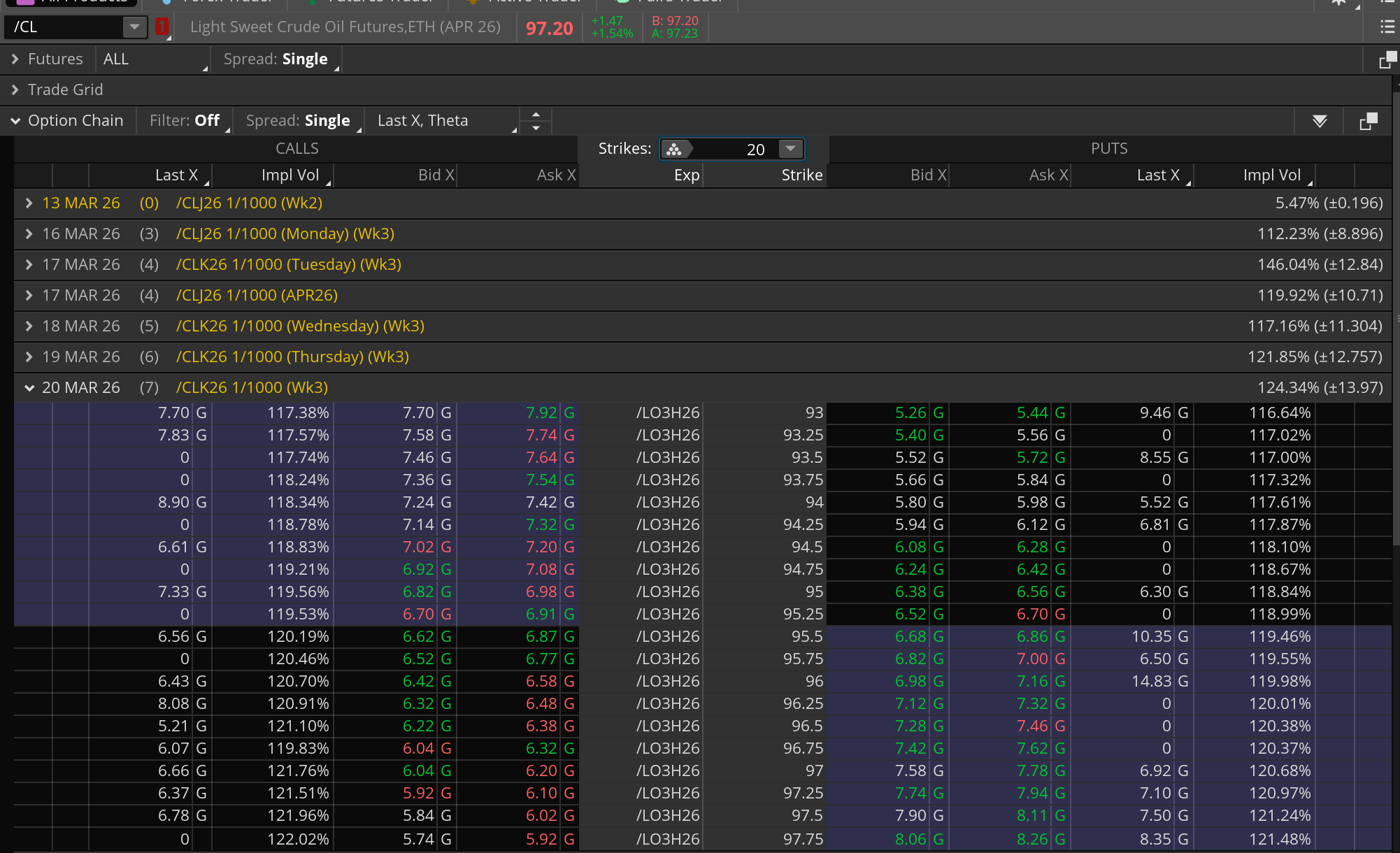

2. Oil Traders Are Bracing for More Big Moves

We took a look at options prices on crude oil futures.

And those prices are high.

Implied volatility on options expiring next Friday is at 120%.

The $97 straddle for next Friday is trading around $13.58 right now.

That's an implied move of about 14% in a single week.

That would seem wild at any other time.

But anything can happen in the Strait of Hormuz, plus the rest of the global oil infrastructure.

3. The Mood Is Going Sour

The latest AAII Sentiment Survey shows that just 31.9% of investors are bullish.

This is the 6th straight weekly decline, and the lowest level since November 12. It's not an extreme reading, but it's below the long-term 37.5% average.

And bearish sentiment jumped to 46.4%, the highest level since November 12.

The CBOE Equity Put/Call Ratio reached 0.80 Wednesday, the highest since February 17. This shows a moderate amount of fear.

It's good to see more caution coming into the market, because by definition, it means there is a lack of froth.

However, these are not extreme measures so we can't use them as an excuse to load the boat with equities.

4. Private Credit Is Coming Into Focus

Many market observers believe the private credit market is the next big market boogeyman.

Private credit grew fast after the financial crisis when traditional banks bulled back on lending to smaller companies.

But now defaults are rising thanks to lax underwriting standards, and there's worry of a crisis brewing.

This has hurt stocks like Blue Owl (OWL), Ares Management (ARES), and even Deutsche Bank (DB), which just disclosed $30 billion in exposure to private credit loans.

And we noticed something funny this week.

Google searches for “what is private credit?” have exploded:

This story is going mainstream.

5. SanDisk Is Amazing

I got stopped out of my SanDisk (SNDK) long last Friday.

So of course it rallied back $100 in under a week. In the middle of a war.

The stock is now up 176% this year, making it the #1 name in the S&P 500 index.

Texas Pacific Land (TPL), the #2 stock, is up “only” 85%.

And SanDisk has two fresh catalysts next week: Micron's (MU) earnings report, and Nvidia's (NVDA) big GTC conference.

Both should point to strong demand for everything related to AI infrastructure, which of course includes flash memory storage.

By the way, JR Romero is sticking to his $1,000 target price:

ATTN: Serious Options Traders

There Is Just ONE Epic Trade Every Week