Headlines Still Rule This Market

We survived another week in this wild market. So here are the 5 things you need to know.

Headlines – and Oil – Still Rule

As Iran and the U.S. reached a two-week ceasefire deal this week… stocks went flying and oil tumbled.

But the good times may have been short lived as concerns about the fragility of the deal came back into the market.

Iran had reportedly agreed to allow safe passage of the Strait of Hormuz but shipping companies said that wasn't happening.

President Trump warned Iran to “stop now” if it was charging tankers to pass through the Strait and ramped up his aggressive tone in a Truth Social post on Friday:

Despite the uncertainty, oil prices ended the week under $100, down nearly 20% from the recent high

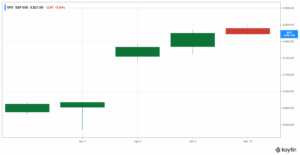

Stocks ended the week with a down day after 4 straight sessions higher, with the S&P 500 up over 3% on the week:

Now we see what happens over the weekend before Monday's open… every day is a risk of a new headline to break things one way or the other.

Consumers Are Feeling Pain

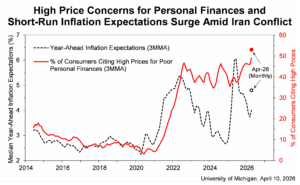

The University of Michigan's preliminary Consumer Sentiment Index plunged to a record low this month as fears mount about rising energy prices and the impact of the Iran war.

The headline index dropped to 47.6 on Friday, down 10.7% from March.

It's the lowest reading on record – even including COVID-era surveys.

That drop coincided with a sharp rise in inflation expectations.

Consumers now see inflation rising 4.8% over the next year, a full 1% higher than March expectations and the highest reading since August 2025.

Most of the interviews for this survey were conducted before the April 7 ceasefire agreement.

So we'll have to watch the release of the final survey for April later this month.

Survey director Joanne Hsu said, “Economic expectations will likely improve after consumers gain confidence that the supply disruptions stemming from the Iran conflict have ended and gas prices have moderated.”

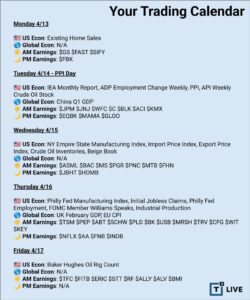

Earnings On Deck

It feels like Q4 earnings season just finally ended… and now we are ramping up for Q1 results.

The action kicks off with the big banks next week, with Netflix (NFLX) being the first big tech company to report.

Here are the highlights:

- Monday AM: Goldman Sachs (GS)

- Tuesday AM: JP Morgan Chase (JPM), Wells Fargo (WFC), Citigroup (C), Johnson & Johnson (JNJ)

- Wednesday AM: Bank of America (BAC), Morgan Stanley (MS)

- Thursday AM: Taiwan Semiconductor (TSM), PepsiCo (PEP), Charles Schwab (SCHW)

- Thursday PM: Netflix (NFLX)

Here's the full calendar for the week, it's pretty quiet besides the Producer Price Index release on Tuesday:

If you want to learn a winning strategy for earnings season, rev up your Earnings Engine with Sami Abusaad!

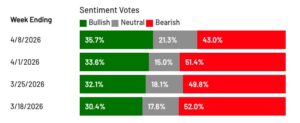

Traders Get More Bullish

The AAII Sentiment Survey shows that 35.7% of investors are bullish.

That's up over 2% from last week, but the 8th straight week of below-average bullishness, though it's not an extreme reading.

Just 43% of investors are bearish, down sharply from 51.4% last week.

While 21.3% are neutral.

These numbers are not shocking considering the tricky environment.

And, over in the options market, things still look pretty neutral.

The CBOE equity put-call ratio has hovered between 0.48 and 0.72 this week.

So the crowd is still pretty cautious.

Hard to pick a direction when you don't know what headline might drop at any moment.

Burry Still Bearish After Trump's PLTR Pump

Palantir (PLTR) was in focus on Friday after President Trump praised the company in a Truth Social post:

After Trump's endorsement of the stock, PLTR bottomed at $122.68 at 10:11am ET before rallying to a high of $129.20 at 11:28am ET.

But “Big Short” investor Michael Burry is still bearish the name.

In a Substack post, Burry wrote, “I now own the June 17 2027 Strike Price 50 Puts and the December 19, 2026 Strike Price 100 Puts. I am not selling these today.”

Even with Friday's pop, PLTR was on track for a roughly 13% weekly drop, bringing the stock's 2026 losses to about 28%.

Burry says the software firm is “wildly overvalued” after peaking near $200 last year.

Meantime, the broader software sector has been hit hard this year with the iShares Expanded Tech-Software Sector ETF (IGV) down nearly 30% YTD.

This earnings season will be key for software stocks to relieve market fears about AI disruptions to their business.

ATTN: Serious Options Traders

There Is Just ONE Epic Trade Every Week